Most people assume “first-time home buyer” means exactly that someone who has never owned a home in their life. The truth is more nuanced, and a lot more generous than most buyers expect.

If you owned a home years ago, then sold it, lost it, or simply walked away from homeownership for a period of time, you may qualify as a first-time home buyer again. And that status matters. It can unlock down payment assistance, lower-rate loan programs, closing cost grants, and other benefits that make a real difference in what you can afford and how quickly you can close.

Whether you’re re-entering the market in Scottsdale after renting for several years, buying solo after a divorce, or moving from investment properties back to a primary residence, this guide covers exactly when your first-time buyer status resets and what you can do with it.

Quick Answer: You are considered a first-time home buyer again if you have not owned or lived in a principal residence during the past three years. This is the standard definition used by the U.S. Department of Housing and Urban Development (HUD) and adopted by most federal loan programs, state housing agencies, and down payment assistance programs across the country including in Arizona.

The 3-Year Rule: The Official Definition That Resets Your Status

Three years. That is the number that matters.

According to HUD’s official definition, a first-time home buyer is any individual who has not owned a principal residence within the past three full years. The clock starts from the date you last owned or lived in a home as your primary residence. When three years pass from that date, your status resets and you can access the same loan programs and assistance available to someone buying for the very first time.

This definition is not just an FHA rule. It is the baseline standard used by Fannie Mae, Freddie Mac, USDA, many state housing finance agencies, and down payment assistance programs across the country. Some programs may have slightly different definitions or additional requirements, but the three-year rule is the near-universal starting point.

The three-year period is calculated backward from the settlement date of your new purchase not from today’s date. So if you are under contract now, lenders look at whether you owned a primary residence any time in the 36 months before your expected closing date.

What Counts as a “Principal Residence” Under HUD’s Definition

A principal residence is the home where you live most of the year. It is the address on your driver’s license, where you receive mail, file your taxes, and spend the majority of your time. This is an important distinction because the type of property you owned previously determines whether that ownership counts against your first-time buyer status.

If you owned and lived in a home as your primary address, that counts. If the home you owned was a vacation property, a rental, or an investment property where you never lived, it generally does not count against your eligibility. The key word in HUD’s definition is “principal” the property has to have been where you actually lived.

What Does Not Count Against Your First-Time Buyer Status

Several categories of prior ownership do not disqualify you from qualifying as a first-time buyer:

- Ownership of an investment property, vacation home, or rental property where you never resided as your primary address

- Living in a home owned by someone else if the property was in a partner’s or parent’s name and you were never on the title

- Owning a mobile home on land you did not own (in many program definitions)

- Owning a property that was deemed uninhabitable or structurally unsafe, where bringing it up to code would have cost more than building or purchasing a new home

The nuances matter, and they vary slightly by lender and program. Your real estate agent and mortgage lender should review your specific history together before assuming you do or do not qualify.

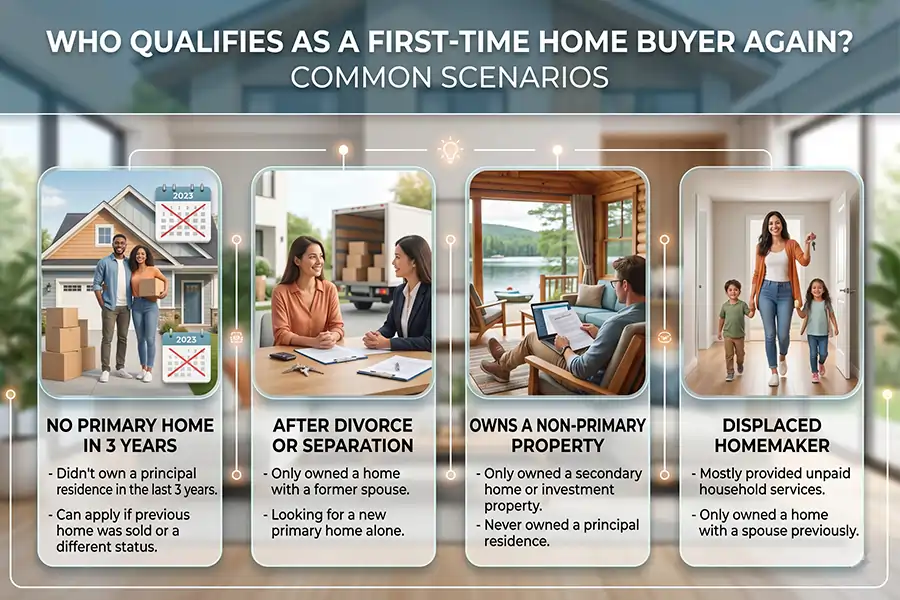

Who Qualifies as a First-Time Home Buyer Again? Common Scenarios

Life rarely follows a straight line, and the programs designed around first-time buyer status recognize that. Here are the most common situations where buyers re-qualify often to their own surprise.

Former Homeowners Who Have Been Renting

This is the most straightforward scenario. If you owned a home, sold it, and have been renting for at least three years since, you qualify as a first-time buyer again under HUD’s definition. The three-year clock started the day your name came off the title.

This applies even if you received equity from the sale. Owning equity in the past does not disqualify you — what matters is whether you currently own, or recently owned, a principal residence.

Divorced or Separated Buyers

Divorce is one of the most common reasons people re-enter the housing market and one of the most frequently misunderstood eligibility situations. If you jointly owned a home with a spouse during your marriage, were removed from the title as part of a divorce settlement, and have not owned another primary residence since, you may qualify as a first-time buyer.

Some programs go further. Bankrate notes that stay-at-home or single parents who jointly owned a marital home but did not solely own the property may qualify as first-time buyers even without the three-year waiting period, depending on the specific program’s guidelines. If you have been through a divorce and are unsure of your status, speak with a lender before assuming you are disqualified.

Displaced Homemakers and Single Parents

HUD’s expanded definition of a first-time home buyer specifically includes displaced homemakers people who have primarily worked in the home (typically caring for family members) and no longer have household income from a spouse — as well as single parents who previously owned only with a former partner. These individuals may qualify as first-time buyers even if the three-year rule is not fully met, depending on the program.

This is one area where working with an experienced local real estate agent makes a measurable difference. Knowing which programs apply to which situations saves time, prevents wrong assumptions, and puts the right opportunities in front of you.

Investment Property Owners Who Never Owned a Primary Home

Here is a scenario that surprises a lot of people: if you own investment properties rental homes, commercial real estate, or vacation properties but have never owned a home that served as your primary residence, you may still qualify as a first-time buyer.

Owning real estate as an investor is fundamentally different from owning a principal residence under most program definitions. If your name is on investment properties but you rent your own living space, you have not triggered the “owned a principal residence” clause. You can still access first-time buyer programs for your primary home purchase.

Buyers Who Lost a Home to Foreclosure or Short Sale

This is another common path back into the market. If you lost a home to foreclosure or a short sale during a financial hardship and three or more years have passed since that event you can re-qualify as a first-time buyer. The three-year rule applies here the same way it applies to any prior ownership situation.

Keep in mind that foreclosures and short sales also affect your credit history and may require additional seasoning periods for certain loan types beyond just the first-time buyer definition. FHA loans, for example, typically require a 3-year waiting period after a foreclosure before you can qualify for a new loan which often aligns with the first-time buyer eligibility window.

What Benefits Can You Access When You Qualify Again?

Re-qualifying as a first-time buyer opens doors that are otherwise closed to repeat purchasers. These benefits are real and financially significant.

FHA Loans With Low Down Payments

The Federal Housing Administration (FHA) loan program is one of the most accessible mortgage options for re-qualifying first-time buyers. You can apply for an FHA loan even if you have had one before there is no lifetime limit on FHA borrowing. What matters is whether you meet the current eligibility criteria.

FHA loans allow down payments as low as 3.5% with a credit score of 580 or higher, and down payments of 10% with scores between 500 and 579. As of 2025, FHA loan limits in Arizona range from $524,225 for single-unit properties up to $1,008,300 for four-unit properties in standard-cost areas, with higher limits applicable in high-cost zones.

The trade-off is that FHA loans require mortgage insurance premiums (MIP) an upfront fee of 1.75% of the loan amount, plus monthly premiums that continue for the life of the loan unless you put down at least 10%.

Conventional Loan Programs: HomeReady and Home Possible

If you want to avoid the long-term MIP of an FHA loan, Fannie Mae’s HomeReady and Freddie Mac’s Home Possible programs offer 3% down payment options with more favorable mortgage insurance terms. Both programs are available to first-time buyers, including re-qualifying buyers who meet the income and credit requirements.

HomeReady requires a minimum credit score of 620. Home Possible requires 660. Both programs have income limits based on area median income (AMI), so your household income relative to your purchase location matters.

USDA and VA Loans

For buyers purchasing in eligible rural or semi-rural areas, USDA loans offer zero down payment financing. The USDA’s definition of a first-time buyer follows similar guidelines to HUD’s, so re-qualifying buyers who meet income and location requirements can access these loans as well.

Veterans and active-duty service members who qualify for VA loans are not limited by first-time buyer definitions at all. VA loans require no down payment and no private mortgage insurance regardless of whether it is your first, second, or third home purchase.

First-Time Home Buyer Programs in Arizona for Re-Qualifying Buyers

Arizona has some of the more robust first-time buyer assistance infrastructure in the country and buyers who re-qualify under the three-year rule can access these programs exactly like any other first-time buyer.

Arizona Home Plus Down Payment Assistance

The Home Plus program, administered by the Arizona Industrial Development Authority (Arizona IDA), offers up to 4% of the loan amount in down payment and closing cost assistance. As of April 2026, the program’s income limit is $155,386 annually. It is available statewide every county, city, and zip code in Arizona and has no sunset date, meaning it does not run out of funds the way many DPA programs do.

To qualify, you need a minimum credit score that varies by loan type, a home buyer education course completion, and the property must be your primary residence. Maricopa County which includes Scottsdale and surrounding areas is fully covered.

Arizona Is Home Program

The Arizona Department of Housing’s Arizona Is Home program defines a first-time homebuyer as someone who has not owned real estate in the last three years precisely matching HUD’s standard. The program provides down payment assistance for buyers in Maricopa and Pima Counties whose income is at or below 120% of the area median income. Assistance comes as a forgivable second mortgage following five years of owner occupancy.

Maricopa County Home in Five Advantage Program

For buyers purchasing in Maricopa County which covers Scottsdale, Phoenix, Arcadia, and surrounding communities the Home in Five Advantage program offers up to 5% assistance for down payment and closing costs. Qualified educators, first responders, veterans, and active-duty service members can receive 6%. Buyers need a minimum credit score of 640 and must meet first-time buyer status under the program’s guidelines.

WISH Grant Program

Through OneAZ Credit Union, eligible first-time buyers in Arizona can access the Workforce Initiative Subsidy for Homeownership (WISH) Grant Program. The program provides up to $32,837 in down payment assistance on a 4-to-1 matching basis for every $1 a buyer contributes, WISH matches $4. Eligibility requires income at or below 80% of the HUD Area Median Income and completion of a homebuyer counseling program. Funds are limited and competitive, so timing matters.

Does Owning an Investment Property Disqualify You?

No owning investment property does not automatically disqualify you from first-time buyer status, as long as those properties were not your primary residence.

This is a critical distinction. If you own rental properties or vacation homes but have been renting your own living space, you have not met the definition of “owning a principal residence.” Under HUD’s guidelines and most program definitions, owning non-primary real estate does not count against you.

That said, some lenders and programs may ask for documentation of your full real estate ownership history. Be transparent about what you own, let your agent and lender review the specifics, and never assume you are disqualified before someone with program expertise has actually reviewed your situation.

How Do You Prove You Qualify as a First-Time Home Buyer Again?

Lenders and assistance programs will verify your prior ownership history through several channels. Being prepared with the right documentation speeds up the process and prevents delays.

Common documentation required to prove first-time buyer eligibility includes:

- Tax returns for the past three years — Tax returns show whether you claimed a mortgage interest deduction, which indicates prior homeownership

- Proof of current living situation — Rental agreements, utility bills, or a letter from your landlord confirming you have been a renter

- Divorce decree or separation agreement — For buyers re-qualifying after a marital property split

- Documentation of property transfer — Closing statements, deed records, or title documents showing when your name was removed from a prior property’s title

- Credit report — Your credit history often reflects prior mortgage activity, which lenders use alongside other documents to verify timing

In some cases, lenders pull public records directly to confirm your ownership history. If your prior home was in another state, be prepared to provide documentation from that transaction, since local county records may not reflect out-of-state ownership history.

Working with an experienced local real estate agent who understands how these programs work and who has connections with lenders that specialize in first-time buyer programs makes this documentation process significantly smoother.

FAQ: First-Time Home Buyer Status Explained

When are you considered a first-time home buyer again?

You are considered a first-time home buyer again once you have not owned or lived in a principal residence for three full years. This is the standard definition used by HUD and adopted by most federal loan programs and state down payment assistance programs in Arizona and nationwide. The three-year window is measured backward from your anticipated closing date.

Can you be a first-time home buyer twice?

Yes. The first-time home buyer designation is not a once-in-a-lifetime status. Under HUD’s definition, you regain it every time you go three consecutive years without owning a principal residence. Some state and local programs may have stricter definitions, but the three-year rule is the federal standard that most programs follow.

Does a divorce qualify you as a first-time home buyer?

It can. If you jointly owned a home with a spouse and your name was removed from the title through a divorce settlement, and you have not owned another primary residence since, you may qualify as a first-time buyer. Some programs extend eligibility to single parents and displaced homemakers even without waiting the full three years. Confirm your specific situation with a lender.

Does owning a rental or investment property disqualify you from first-time buyer programs?

Generally, no. Investment properties, vacation homes, and rentals do not count as a principal residence under HUD’s definition. If you have only owned non-primary real estate and have been renting your own home, you may still qualify as a first-time buyer for a primary residence purchase.

Can you get an FHA loan as a first-time buyer again?

Yes. There is no lifetime limit on FHA loans, and you can apply for one as a re-qualifying first-time buyer. You must meet the current FHA eligibility criteria: a minimum 580 credit score for 3.5% down, or 500-579 for 10% down. You cannot have more than one active FHA loan at a time, but having used one previously does not disqualify you from using another.

Does a foreclosure reset your first-time buyer status?

Yes, if three or more years have passed since the foreclosure was completed and you have not owned another primary residence since then. Keep in mind that FHA loans also require a standard 3-year waiting period after a foreclosure before you can qualify for a new loan, so these timelines often align. Some conventional programs have different waiting periods, so check requirements by loan type.

What first-time home buyer programs are available in Arizona?

Arizona offers several programs for re-qualifying first-time buyers, including the Arizona Home Plus program (up to 4% down payment assistance statewide), the Arizona Is Home program (Maricopa and Pima Counties), the Maricopa County Home in Five Advantage program (up to 5-6% assistance), and the WISH Grant Program through OneAZ (up to $32,837 in matching assistance). All use HUD’s three-year definition to determine eligibility.

How do you prove you qualify as a first-time buyer again?

Lenders verify eligibility using your tax returns from the past three years, rental agreements or other proof of your current living situation, documentation of when you last sold or transferred ownership of a primary residence, and sometimes your credit report, which reflects prior mortgage activity. For divorce situations, a decree or separation agreement showing when you were removed from the title is typically required.

Closing

Qualifying as a first-time home buyer again is not a loophole it is a feature of how the housing finance system was designed. Life changes. People sell homes, go through divorces, lose properties, move for work, or simply spend years renting while their circumstances stabilize. The three-year rule exists to ensure that the programs built for first-time buyers remain accessible to people who genuinely need a fresh start.

In Arizona’s market where the median home sale price in Scottsdale sits near $861,000 and even Phoenix-area entry-level properties are testing buyers’ budgets the down payment assistance and favorable loan terms available to first-time buyers can make a decisive difference in what you can afford and when you can close.

If you think you may qualify, do not guess. Speak with a lender who knows Arizona’s first-time buyer programs, and work with a real estate agent who understands how to structure your purchase around the programs that fit your situation.

Reach out to Kelly Jones for a personalized consultation. With deep expertise in Scottsdale, Paradise Valley, Phoenix, and Arcadia, Kelly helps buyers at every stage including those returning to homeownership after time away navigate the Arizona market with clarity and confidence.